This product was not featured by Product Hunt yet. It will not be visible on their landing page and won't be ranked (cannot win product of the day regardless of upvotes).

Product upvotes vs the next 3

Waiting for data. Loading

Product comments vs the next 3

Waiting for data. Loading

Product upvote speed vs the next 3

Waiting for data. Loading

Product upvotes and comments

Waiting for data. Loading

Product vs the next 3

Loading

Arera

Underwriting Infrastructure for NBFCs & Lenders

Arera provides deterministic, rules-based underwriting infrastructure for NBFCs. Automate bank statement analysis, credit decisioning, and loan origination. RBI-compliant, explainable, and audit-ready. Live at tryarera.com.

Honestly? A phone call with a friend who works at an NBFC in Delhi.

He was venting about his day 200 loan applications sitting in his queue, each one a PDF he had to open manually, look for salary credits, eyeball the EMI pattern, and type a recommendation into a spreadsheet. He'd been doing this for 8 hours straight.

I asked him how long it takes to decide on one application. He said 'good ones take 20 minutes, bad ones take longer because I have to write up the rejection properly.'

I asked what happens when he's tired or distracted. He paused and said 'honestly the afternoon ones get less attention.'

That stuck with me. Someone's loan approval their ability to start a business, handle a medical emergency, send their kid to college was partially determined by whether a credit analyst had eaten lunch yet.

That's not a people problem. That's an infrastructure problem. And I couldn't stop thinking about it.

India has 10,000+ registered NBFCs. Every single one underwrites loans manually.

But the problem isn't just speed it's defensibility. In 2022 RBI passed Digital Lending Guidelines that require every regulated lender to produce explainable, auditable credit decisions. Meaning when a borrower disputes a rejection, the NBFC needs to show exactly which rule triggered it, what data it was based on, and which version of their policy was active at that moment.

Manual processes can't produce that. Neither can AI black boxes 'the model said no' isn't a regulatory answer.

So there's this gap: regulation is forcing lenders toward explainability, but no infrastructure exists to deliver it.

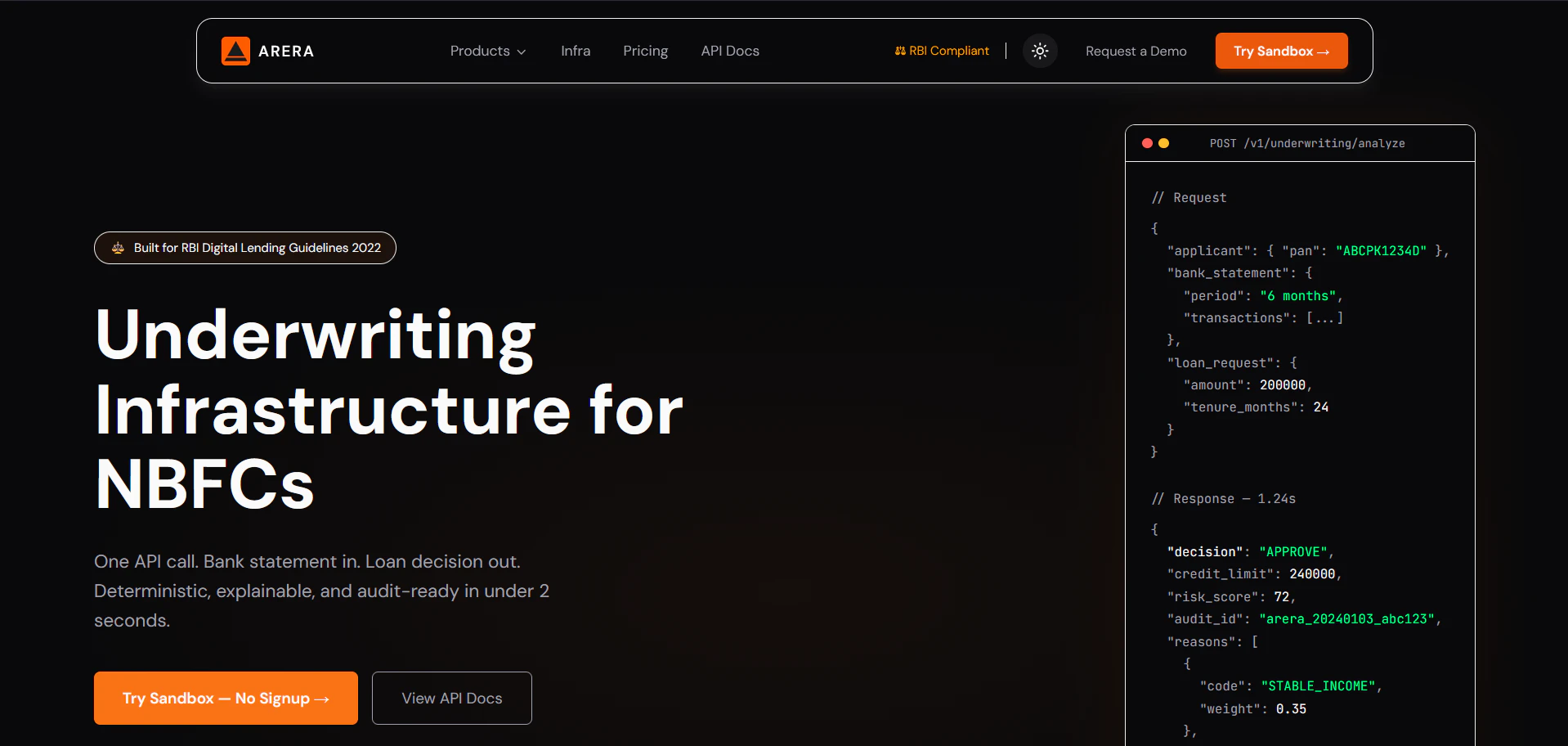

Arera is that infrastructure. One API call. Bank statement in. Loan decision out. Every rule that fired, every reason weighted, an immutable audit ID all of it structured to be printable in a regulatory filing on day one.

The credit analyst doesn't disappear. They just stop doing the part that should never have been human in the first place.

I started thinking it was an AI problem. Everyone in fintech was building GPT wrappers for underwriting. I almost did the same.

Then I read RBI's actual circular RBI/2022-23/111 in full. Not a summary, the whole thing. And I realized the regulation was describing exactly the kind of system that AI can't build. It needs to be deterministic. Consistent. Auditable. The same input must always produce the same output with the same explanation.

That's when the product completely changed direction. I stopped thinking 'how do I make a smarter model' and started thinking 'how do I build infrastructure a regulator would actually accept.'

The first version was just the rules engine 24 policies, income thresholds, EMI ratios, salary regularity. No UI, no dashboard, just a Node.js endpoint that returned a JSON decision.

I showed that raw API response to a credit manager at an NBFC. She didn't ask about accuracy or features. She asked: 'Can we plug this into our loan management system?'

That one question told me everything. She didn't want a product. She wanted a primitive something to plug into what already exists.

So I built backward from that. The API stayed the same. I added the audit trail, the explainability output, the webhook delivery, the developer playground everything structured around that one integration question.

The AI parser came last. Real NBFCs don't send clean JSON they have PDFs from 12 different banks all formatted differently. So I added Claude as a parsing layer that sits before the rules engine. AI handles the messy input. Deterministic logic makes the decision. Clean separation.

Built the whole thing solo in 4 weeks. Launching here to find the first NBFCs who want to run a pilot.

If you're in lending in India or know someone who is, I'd love to talk.

About Arera on Product Hunt

“Underwriting Infrastructure for NBFCs & Lenders”

Arera was submitted on Product Hunt and earned 4 upvotes and 1 comments, placing #141 on the daily leaderboard. Arera provides deterministic, rules-based underwriting infrastructure for NBFCs. Automate bank statement analysis, credit decisioning, and loan origination. RBI-compliant, explainable, and audit-ready. Live at tryarera.com.

On the analytics side, Arera competes within Fintech, Artificial Intelligence and Money — topics that collectively have 527.5k followers on Product Hunt. The dashboard above tracks how Arera performed against the three products that launched closest to it on the same day.

Who hunted Arera?

Arera was hunted by Harshit Arora. A “hunter” on Product Hunt is the community member who submits a product to the platform — uploading the images, the link, and tagging the makers behind it. Hunters typically write the first comment explaining why a product is worth attention, and their followers are notified the moment they post. Around 79% of featured launches on Product Hunt are self-hunted by their makers, but a well-known hunter still acts as a signal of quality to the rest of the community. See the full all-time top hunters leaderboard to discover who is shaping the Product Hunt ecosystem.

For a complete overview of Arera including community comment highlights and product details, visit the product overview.

Harshit Arora

Harshit Arora